In the high-stakes arena of global energy logistics, few figures possess the deep-rooted expertise of those navigating the volatile waters of the Middle East. As the maritime industry grapples with shifting geopolitical alliances and the rapid evolution of liquefied natural gas (LNG) transport, understanding the balance between operational resilience and aggressive expansion is crucial. This discussion delves into the strategic maneuvers required to maintain profitability when regional tensions threaten the world’s most vital energy corridors, exploring how one of the world’s largest shipping fleets manages to thrive despite unprecedented infrastructure challenges and shifting market demands.

The following conversation explores the mechanisms of long-term financial stability, the logistical realities of operating through the Strait of Hormuz during periods of blockade, and the technical hurdles of integrating next-generation vessels into a global fleet. We also examine the impact of significant capacity losses and the forward-looking strategies aimed at capturing a massive projected surge in global liquefaction capacity by the end of the decade.

Net profits rose to QAR 439 million in early 2026 despite significant regional volatility. How did your long-term charter contracts specifically insulate these earnings from market swings, and what metrics do you use to evaluate the risk-adjusted returns of these high-quality agreements?

The stability we achieved, climbing from QAR 375 million in the final quarter of 2025 to QAR 439 million today, is no accident; it is the direct result of a “fortress” balance sheet built on multi-decadal commitments. These long-term, high-quality charter contracts act as a financial shock absorber, ensuring that even when spot market sentiment turns sour or regional tensions flare, our cash flow remains predictable and shielded from the immediate chaos. We evaluate these agreements by looking closely at the counterparty’s credit duration and the “yield-to-delivery” ratio, which ensures that each hull in our fleet is earning its keep regardless of the day-to-day fluctuations in the Arabian Gulf. There is a profound sense of security that comes from knowing your fleet is spoken for years in advance, allowing our leadership to focus on navigation and safety rather than chasing the next available cargo in a panicked market. It is this disciplined approach to revenue locking that has allowed us to consistently outperform the previous year’s first-quarter benchmark of QAR 433 million.

Operations at dry docks and towing services have seen noticeable declines in activity recently. What specific expense-rationalization measures were implemented to offset these lower operating rates, and could you walk us through the step-by-step process of identifying which service sectors required the most immediate cuts?

When we noticed the operating rates for our agency and towing services dipping, we immediately initiated a “zero-base” review of our auxiliary maritime divisions to prevent a margin squeeze. This process began with a granular audit of our dry dock labor shifts and fuel consumption for tugboats, identifying that the drop in vessel traffic through certain corridors made our previous staffing levels unsustainable. We moved quickly to consolidate maintenance schedules, delaying non-essential capital expenditures at our repair facilities while cross-training our towing crews to handle broader logistical roles. It was a difficult but necessary period of tightening the belt, where we felt the weight of every idle crane and quiet dock, yet these rationalization measures were the only way to protect the bottom line from the “noticeable decline” mentioned in our performance reviews. By reacting with speed to align our overhead with the current volume of regional traffic, we effectively neutralized the negative impact that these slower business sectors could have had on our overall quarterly success.

Transit through the Strait of Hormuz remains a critical bottleneck during periods of regional blockade. How has your operational team adjusted vessel routing or insurance strategies to maintain maritime links, and what anecdotes can you share regarding the logistical hurdles of navigating these high-tension zones?

Navigating the Strait of Hormuz since the blockades began in late February has required a level of tactical precision that feels more like a military operation than standard commercial shipping. Our teams have had to engage in “dynamic rerouting,” constantly communicating with international naval monitors to find safe windows for our 69 active LNG carriers to slip through the bottleneck. The stress in the operations room is palpable when a vessel approaches the strait; we’ve seen insurance premiums for “war risk” skyrocket, forcing us to renegotiate coverage terms almost on a voyage-by-voyage basis to keep costs from spiraling. I recall a particular instance where a captain had to hold position for forty-eight hours just outside the zone, managing crew anxiety while waiting for a clear corridor to open—a vivid reminder that in this part of the world, geography is often our most stubborn adversary. Despite these hurdles, our maritime links remain unbroken because we have prioritized real-time intelligence and localized risk assessment over traditional, static passage plans.

Recent attacks have reportedly sidelined 17% of local LNG capacity for the next several years. How does this significant infrastructure loss impact your immediate vessel deployment schedules, and what specific adjustments are being made to fulfill existing delivery commitments during this five-year recovery period?

The loss of 17% of our national LNG capacity is a staggering blow that has forced us to completely redraw our deployment maps for the foreseeable future. With a significant portion of our expected cargo offline for up to five years, we are shifting our vessels to support international “swing” producers and focusing on optimizing the utilization of our existing 72-ship fleet. We are currently engaged in a complex “cargo swapping” program where we coordinate with global partners to fulfill our delivery commitments using supply from alternative regions, reducing the ton-mile pressure on our local terminals. The sight of idle loading arms at the damaged facilities is a somber reminder of our vulnerability, but it has also spurred us to be more creative in how we bridge the supply gap through third-party charters and enhanced ship-to-ship coordination. Our priority remains honoring every single contract, and we are working tirelessly to ensure that the five-year recovery window does not result in a single missed delivery for our global customers.

The fleet is projected to grow to 112 vessels, including specialized QC-Max and ammonia carriers. What technical challenges arise when integrating these massive newbuilds into an active fleet, and how do you plan to train crews to handle the unique safety requirements of the new LPG/ammonia ships?

Expanding our fleet to 112 vessels is a massive undertaking, particularly with the introduction of the QC-Max—the largest LNG carriers ever built—which require specific berthing depths and advanced cooling technologies. The technical challenge lies in the sheer scale of these ships; they don’t just carry more cargo, they behave differently in heavy seas and require entirely new port protocols to manage their massive displacement. For the four new LPG/ammonia carriers, the stakes are even higher due to the toxic and corrosive nature of ammonia, necessitating a rigorous, simulated training program for our crews that focuses on advanced leak detection and emergency pressure management. We are investing heavily in high-fidelity bridge simulators and cryogenic handling workshops to ensure our seafarers feel confident and safe before they ever step onto the deck of these specialized ships. It is a transition that requires a total shift in our safety culture, moving from standard methane handling to the more complex chemical profiles of the future energy mix.

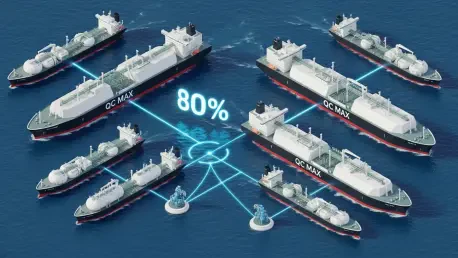

Global liquefaction capacity is expected to surge by 80% through 2031. Beyond simply adding more hulls, what strategic investments are you making in ship-to-ship transfer technology or decarbonization to stay competitive as spot and multi-month charter rates continue to climb?

With the world’s liquefaction capacity set to explode by 80% over the next several years, we recognize that having the most ships won’t be enough if those ships aren’t the most efficient and versatile on the water. We are aggressively investing in “Sub-Cooler” technologies and advanced boil-off gas management systems to ensure that we deliver the maximum amount of energy with the minimum amount of waste, especially as charter rates for one-year and multi-month contracts continue their upward trend. Our decarbonization roadmap includes trialing wind-assisted propulsion and carbon capture systems on our newer hulls to meet the increasingly stringent environmental demands of our European and Asian off-takers. Furthermore, we are refining our ship-to-ship (STS) transfer capabilities to allow for more flexible delivery in regions without deep-water ports, essentially turning our fleet into a floating, mobile pipeline. These investments ensure that as the market grows, we remain the partner of choice for those who value technical sophistication and environmental stewardship as much as they value reliability.

What is your forecast for the Qatari LNG shipping sector?

I believe the Qatari LNG shipping sector is entering a “Golden Age of Resilience” where we will see a decoupling of profitability from regional instability. Despite the current 17% capacity setback, the sheer scale of the global demand surge—that 80% increase in liquefaction by 2031—means that every one of our 112 planned vessels will be essential to global energy security. We will likely see a permanent shift toward higher-capacity vessels like the QC-Max and a diversifying fleet that handles ammonia as a primary clean fuel, positioning Qatar not just as a gas exporter, but as a total energy logistics hub. While the geopolitical shadows in the Strait of Hormuz may persist, our ability to innovate through these pressures will define the next decade, making the Qatari fleet the most technologically advanced and indispensable link in the global energy chain.